Over the years, the Cleantech space has faced its fair share of headwinds. Investors have often walked a rocky path, with a lack of good returns, high risk, regulatory complexities, and other barriers preventing the energy transition from taking place smoothly. The first Cleantech Boom of 2006-2011 led to staggering losses. In five years alone, over half of the $25 billion invested in Cleantech startups evaporated. Since then, the winds have changed. Technologies have improved and international commitments from companies and governments have reduced risk.

Cleantech remains a crucial sector for early-stage investors – replete with unique challenges. Keith Gillard, CEO of UpperStage. Capital brings over two decades of impact investment experience. According to him, driving impact and top-tier investments in Cleantech is possible if investors can recognize certain signs before writing that check.

Decoding Cleantech, Impact and ESG

The term ‘Cleantech’ was coined in the early 2000s by investor and entrepreneur Nicholas Parker to market his conferences. Around the same time, Keith was managing Mitsubishi's venture capital activities in Canada. After the Dot Com Bubble burst, he shifted focus towards Vancouver’s burgeoning fuel cell scene. Since then, he has spent years raising funds, making deals, and following trends in the clean energy space.

There remains a lot of confusion around Cleantech-related terms — ‘Impact’ and ‘ESG’ are prime examples of this. Keith says the two concepts overlap but differ in essence. The impact can be understood as the actual impact a company’s products or services have on the world. It can be scaled by calculating the per-unit impact of all the products a company sells.

ESG, or Environmental Social and Governance, Keith says, is the impact the world has on a company. It is best thought of as a measure of risk. Investors need to care about each pillar of ESG, adds Keith, not because it is the right thing to do but because in five or ten years, when these risks will be priced into deals, an investor's ability to exit may be affected.

Signs of Life in Cleantech

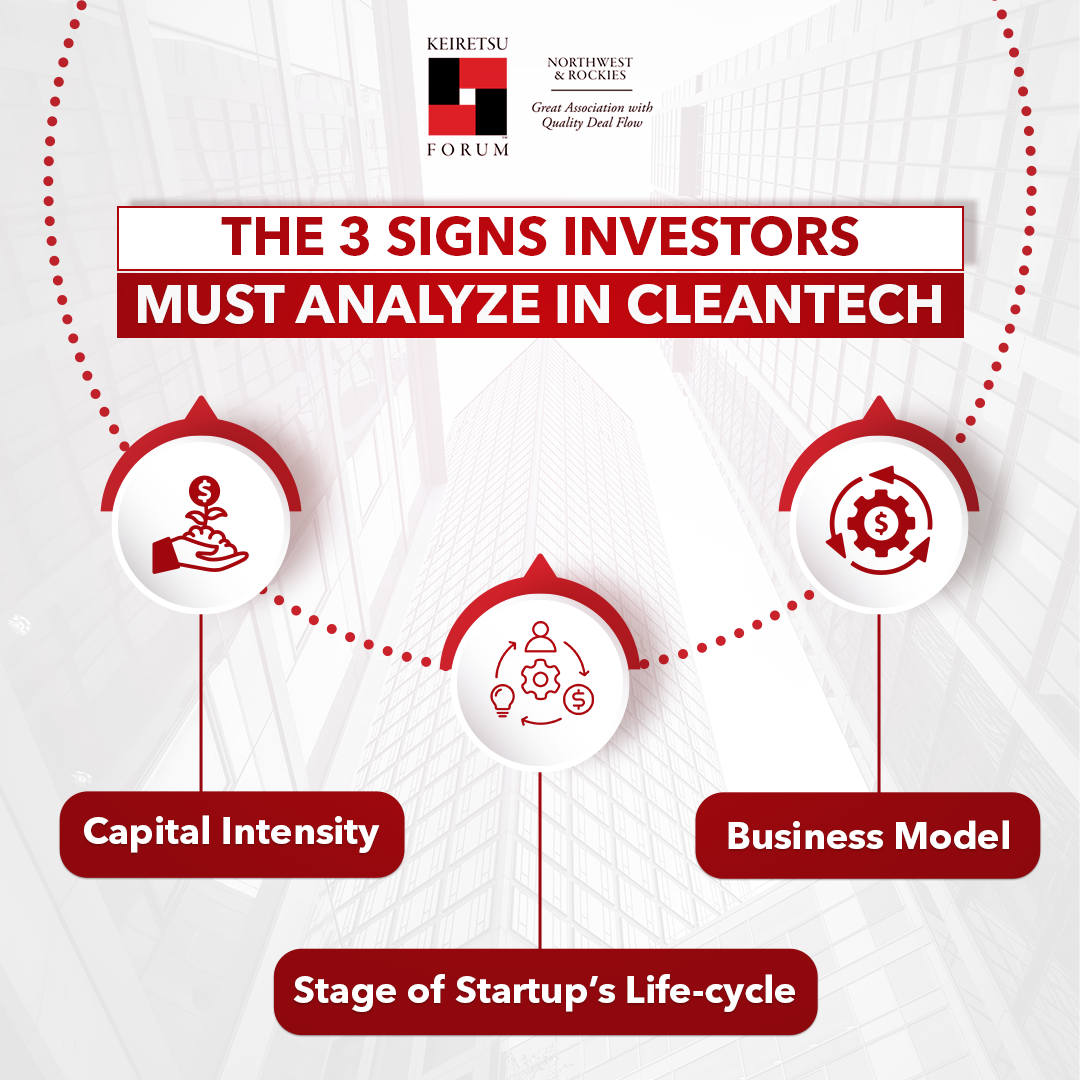

A 2015 Cambridge Associates report contained some startling details on how their Cleantech portfolio had performed. In the early-stage, the pooled IRR was a measly 0.5%. In late-stage, it was up to 9.5% — not bad, but still poor compared to late-stage IT or Life Sciences. However vexing these numbers may appear, they do tell a story. Keith says there are two other indicators that investors could latch on to as a measure of what could perform well.

The first indicator is Capital Intensity — simply put, the more money invested, the more money needed to generate the same returns. American Cleantech results have lagged because the most capital-intensive plays took place in the US. The losses of bigwigs like Solyndra were so tremendous and produced such strong effects that the signals of lower capital intensity plays (which gave good returns) disappeared. Lower capital intensity correlated with better performance in the rest of the world.

The other signal, surprisingly, is the Business Model. Keith says the traditional way is for many Cleantech companies to sell 'widgets' or products with a per-unit cost, for example, biofuels. However, in his experience, the companies that did well were not just selling a product but presented themselves as a service model with recurring subscription revenue. A great example of this, he recalls, is CarbonCure – a company Keith has been involved with in the past. This is how they pivoted using an approach similar to Tetrapak’s business model.

‘Packing’ Value in The Service Model

Today, Tetrapak is a well-known food processing and packaging company. Back in the day, when the brand wasn’t as big, it had to deal with problems getting its product adopted. What it would do next would change the game. The company decided to provide food manufacturers the Tetrapak hardware for free and installed it at their factories at no cost. They faced a CapEx hit upfront. But their customers were in the black because they did not need the capital outlay to adopt the new, superior technology. Customers adopted the solution much faster and didn’t need to amortize it over time.

CarbonCure did that as well. At first, it sold bricks and mortar stones infused with CO2, but after Keith’s investment, it pivoted from selling stones to selling big machines. The company went the Tetrapak way and provided their machinery to cement makers like Lafarge for free. Once it did this, it provided a service and charged the companies per cubic meter of concrete manufactured using CarbonCure’s process. Examining the data available, the company was able to monitor the exact cement savings and tweaked its pricing for the right balance. Customers loved it and the concept mushroomed.

While the capital intensity problem reared its head early, the issue was resolved in months. When it became clear that the model was working, equipment finance companies were ready to finance the installation costs. Thus, the impact of CarbonCure footing that initial bill was reduced –– with a third party willing to do it for them. Keith says, "Everybody won. There was great alignment between the technology provider, the end customer, and a financial middleman that was able to put it together.”

If an investor is mulling over a Cleantech company and their offering aligns with customers and themselves – where a win for one is a win for both – it is a clear sign that there could be potential in that model.

In Vancouver, one of the birthplaces of Cleantech, Keith has been a founding director of Foresight, Canada’s largest Cleantech accelerator. They have over 1,000 client companies going through their programs and more constantly coming in. While many of these startups look for funding, all of them could use help and investor mentorship. Keith urges investors to get involved with Foresight and work with these companies to provide them with some guidance and support. In return, there could be something valuable for the investors. As he signs off, he says, “There are probably some opportunities in there that [could] really excite you".

About the Speaker

Keith Gillard is a seasoned impact investor with over two decades of experience, currently serving as the co-founder and CEO of UpperStage.Capital Inc., an impact-focused private equity firm dedicated to propelling profitable companies to new heights. His extensive career includes leadership roles on the boards of numerous companies, funds, and nonprofit organizations. Keith is renowned for his fundraising prowess, deal-making expertise, and extensive global network, fostering close relationships with multinational organizations and leading investors across North America, Asia, and Europe. He co-founded and chairs Foresight Canada, the country's largest Cleantech accelerator, and is actively involved in various organizations and advisory boards, contributing significantly to impact investing. Outside of his professional life, Keith is a devoted father of three, an avid cyclist, and a two-time Canadian Independent Music Award nominee.

To watch Keith’s entire talk on Keiretsu Forum TV, visit: https://keiretsuforum.tv/cleantech-lessons-learned-driving-impact-and-toptier-investment-returns-with-keith-gillard/