Every dollar matters in the early stages of a company. A large chunk of money goes into building software, testing formulas, or iterating on prototypes. During this stage, the Internal Revenue Service (IRS) rewards your innovation through Research & Development (R&D) tax credits.

Since the PATH Act of 2015, startups with under $5 million in gross receipts and less than five years of revenue history can apply the R&D credit against their payroll taxes (up to $500,000 per year) rather than income taxes, which is massive if you're yet to register a profit. But the IRS doesn't hand it out loosely.

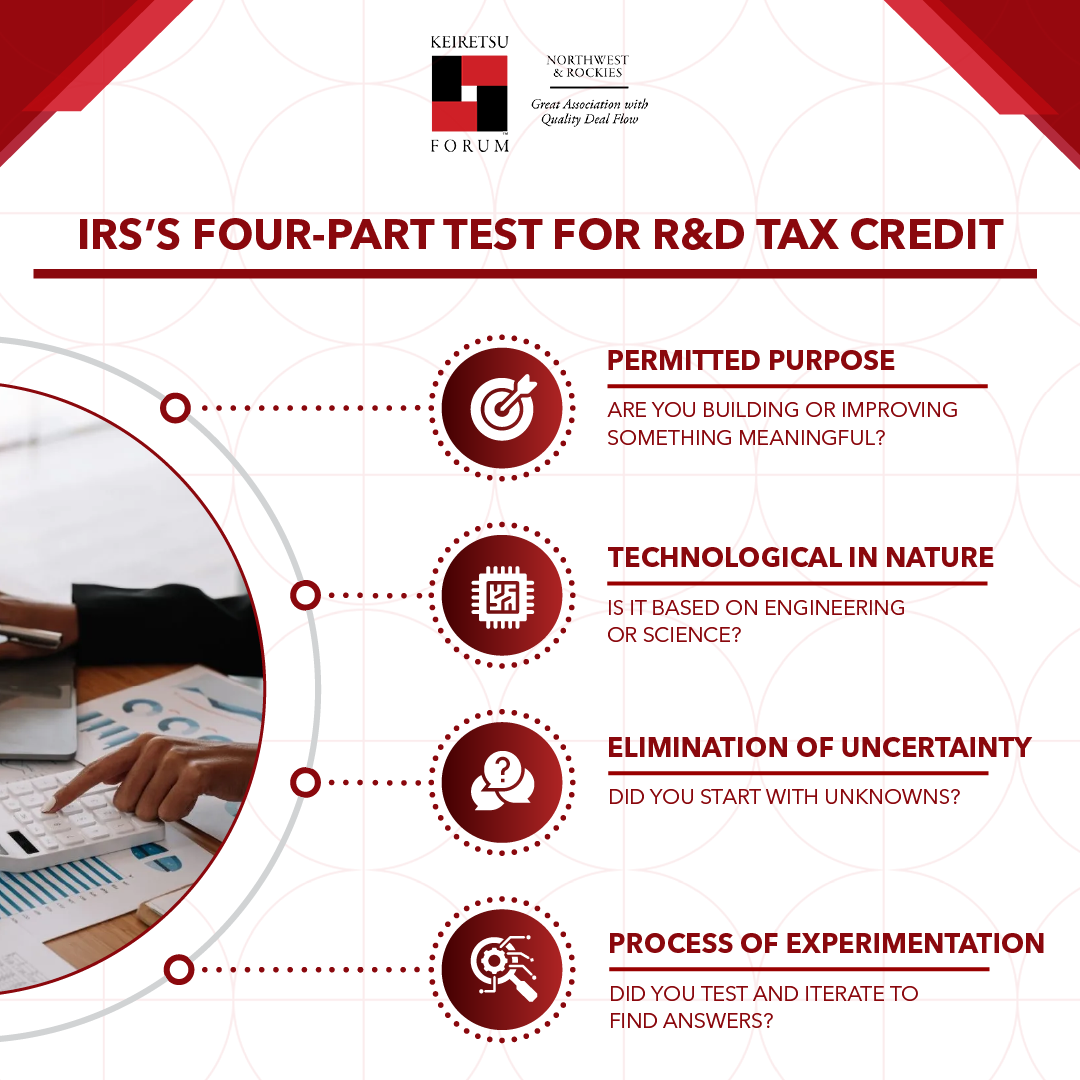

At the heart of this credit is the Four-Part Test defined by the IRS. If your business activities pass this test, you may qualify for significant tax savings. You don't need to be a lab-coat company. SaaS platforms, hardware startups, food-tech companies, and even construction-tech firms have successfully claimed this credit.

Here's what that test actually means, with examples your accountant won't need to translate.

Part 1: Permitted Purpose

Definition: The activity must relate to developing a new or improved business component — meaning a product, process, software, technique, formula, or invention intended for sale or use in your business.

The first point of the checklist verifies if your business ties to something functional—whether it's a product you're building, a tool that powers your operations, or a core process your business depends on. Activities like high-level strategy discussions, market research, or customer discovery, while critical to building a company, do not fit the bill.

Imagine you're developing a route-optimization algorithm for a logistics startup. The algorithm itself is a functional business component, so writing, testing, and improving that code qualify as permitted purposes. However, a meeting in which the team debates whether to build the algorithm does not meet the criteria.

It's also important to distinguish between functional improvements and cosmetic changes. If your solution solely focuses on tailoring a product to a specific customer's preferences, such as adjusting colors, styling, or other aesthetic elements, it does not qualify for the tax credit. As said above, aim for something functional, an improvement over a process, or something along those lines.

Part 2: Technological in Nature

Definition: The activity must fundamentally rely on principles of the hard sciences — engineering, physics, chemistry, biology, or computer science.

The second part requires the business to be grounded in a scientific or engineering discipline, not just business creativity or artistic judgment. Saying "we experimented with a new marketing approach" doesn't meet that bar. On the other hand, "we developed a machine learning model to improve our recommendation engine" is what IRS is looking for.

Consider a food-tech startup working on fermentation techniques to extend shelf life. The solution draws directly on biology and chemistry, making it a technological solution. In contrast, a beverage company running A/B tests on label designs is operating in the marketing space, not science or engineering.

Software development comes under computer science, but there's an important distinction. Building new software or engineering meaningful enhancements generally qualifies, while simply configuring or customizing off-the-shelf tools is not considered "technological". For example, tweaking a Shopify theme will not qualify you for the tax credits. Developing a custom inventory-routing engine from the ground up, however, ticks the right boxes.

Part 3: Elimination of Uncertainty

Definition: The activity must be intended to discover information that would eliminate technical uncertainty — uncertainty about whether something can be built, how it should be designed, or whether it will work at all.

The third part requires you to tackle genuine technical uncertainty. If a solution is already well understood and you're simply executing it on a different platform, the idea won't qualify.

Let's say you are exploring whether a neural network can reliably detect equipment wear using data from wearable sensors. Nobody knows for certain whether the model will reach acceptable accuracy thresholds — that's legitimate technical uncertainty. However, testing if a payment gateway charges the right amount is a validation exercise, not a technical uncertainty.

Pro tip: Be sure to document the technical questions your engineers and developers are trying to answer at the outset of a project. Statements like, "We weren't sure whether approach X would achieve performance threshold Y," can be incredibly valuable, especially if you ever need to substantiate your work during an audit.

Part 4: Process of Experimentation

Definition: The activity must involve a process of experimentation — evaluating alternatives through modeling, simulation, systematic trial-and-error, or hypothesis testing to resolve the uncertainty in Part 3.

You need to show that you encountered challenges in building your solution. You tried approach A, evaluated it, and finally pivoted to approach B.

Take a med-tech startup developing a wearable device. If the team tests multiple sensor placements to determine which yields the most reliable biometric data, each configuration represents a hypothesis. The process of evaluating and comparing those outcomes aligns closely with what the IRS looks for.

If your engineers followed a known blueprint, even a complex one, without meaningful uncertainty or course correction, the IRS may argue that your solution involved no experimentation.

The Bottom Line

The Four-Part Test of the IRS rewards genuine innovation. If your team is technically solving hard problems, iterating through uncertainty, and building something new, there's a good chance you qualify for the tax credits. Use the above points as a checklist and analyze if your business meets all four requirements.

The biggest mistake most early-stage entrepreneurs make isn't failing the test; it's never attempting to document and claim it in the first place. Start tracking now, and talk to a tax professional who specializes in R&D credits before your next filing.